Fractals in time - Day 2

Characteristic features of fractals

-

Mandelbrot Originally defined fractals as sets that have fractal dimension strictly greater than its topological dimension.

-

There is no hard and fast definition but a list of properties.

-

We refer to F as fractal if:

-

F has a fine structure: i.e. detail on small scales.

-

F is too irregular to be described by traditional geometrical language

-

F has some form of self-similarity, perhaps approximate or statistical

-

Usually the fractal dimension of F is greater than its topological dimension

-

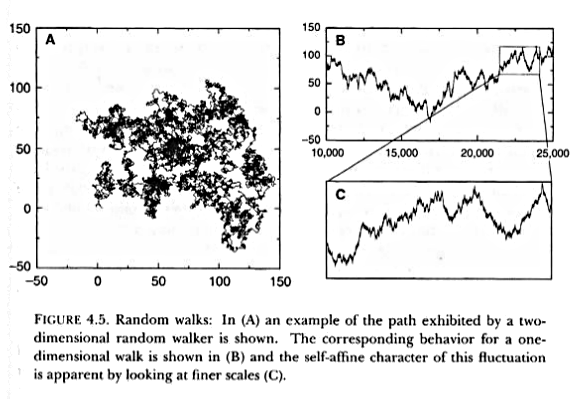

Random walks

-

Random walk (RW) is a stochastic process in which an object moves in a space by performing random jumps

-

We can see that the enlarged view of a small part of the trajectory looks similar to the original, is fractal.

-

The pattern displayed by the one dimensional RW is not self-similar but self-affine because the time and space dimensions do not scale in the same way

Fractal time series

-

Fractal properties in time series can be analyzed by means of Hurst’s Rescaled Range Analysis

Let us consider a time series that can be: the number of extinctions of a group of organism or a particular population or the discharge of a river, etc.

$X_i$ with $i=1,2,3,…,T$

The average of $X_i$ over $T$ time steps will be $< X >T = \left( \sum{i} X_t \right)/T$

The departure from the average over a t-year time horizont is given by:

$$X(t,T) = \sum_{i=1}^{t} [X_i - < X >T ] = \left( \sum{i=1}^{T} X_i \right) - t < X >_T$$

$X(t,T)$ is usually calculated dividing the time series in $M$ segments of size $T$.

-

What is the value of $X(T,T)$ ?

Rescaled Range Analysis

-

We need to calculate two more quantities from the previous :

The standard deviation $S(T) = \left( (< X_t - < X >_T >)^2 \right)^{1/2}$

The range $R(T) = \max_{1 \le t \le T} X(t,T) - \min_{1 \le t \le T} X(t,T)$

-

The rescaled range is: $F(T)=R(T)/S(T)$

-

Calculate $F(T)$ using $T=5$ and the following series

3 4 9 2 1 7 8 2 2 9 -

When the values of the time series are uncorrelated $F(T) \propto T^{1/2}$, which is called white noise. The best predictor is the last measured value.

-

Hurst found a more general scaling relation $F(T) \propto T^{H}$.

for the natural systems he analyzed $H > 1/2$

it can be shown (easily) than the fractal dimension is related:

$$D = 2 - H$$

-

When the Hurst exponent is greater than 1/2 the system shows persistence on all time scales. An increasing trend in the past implies an increasing trend in the future.

If $H < 1/2$ an increase in the past implies a decrease in the future, the system shows antipersistence.

Papers

We will analyze the data from the paper:

- Meltzer MI, Hastings HM (1992) The use of fractals to assess the ecological impact of increased cattle population: case study from the Runde Communal Land, Zimbabwe. Journal of Applied Ecology 29: 635–646.

Leonardo A. Saravia

Professor/Researcher

Investigador Independiente CADIC - CONICET, Docente/Investigador de la UNGS, Doctor en Biología de la UBA. Complex systems. Networks. Global Forest Fragmentation. Open science. R, Julia, Netlogo, C++ & Python.